Paul’s charge to us in Romans 13:8 to owe nothing but love is a powerful reminder of God’s distaste for all forms of debt that are not being paid in a timely manner (see also Psalm 37:21). At the same time, the Bible does not explicitly command against all forms of debt. The Bible warns against debt, and extols the virtue of not going into debt, but does not forbid debt. The Bible has harsh words of condemnation for lenders who abuse those who are bound to them in debt, but it does not condemn the debtor.

Some people question the charging of any interest on loans, but several times in the Bible we see that a fair interest rate is expected to be received on borrowed money (Proverbs 28:8; Matthew 25:27). In ancient Israel, the Law did prohibit charging interest on one category of loans—those made to the poor (Leviticus 25:35-38). This law had many social, financial, and spiritual implications, but two are especially worth mentioning. First, the law genuinely helped the poor by not making their situation worse. It was bad enough to have fallen into poverty, and it could be humiliating to have to seek assistance. But if, in addition to repaying the loan, a poor person had to make crushing interest payments, the obligation would be more hurtful than helpful.

Second, the law taught an important spiritual lesson. For a lender to forego interest on a loan to a poor person would be an act of mercy. He would be losing the use of that money while it was loaned out. Yet that would be a tangible way of expressing gratitude to God for His mercy in not charging His people “interest” for the grace He has extended to them. Just as God had mercifully brought the Israelites out of Egypt when they were nothing but penniless slaves and had given them a land of their own (Leviticus 25:38), so He expected them to express similar kindness to their own poor citizens.

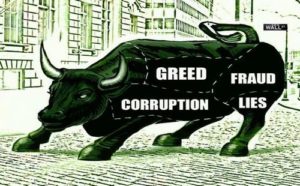

From manipulating rates to mis-selling products and lax enforcement of money-laundering controls, the scandals in the financial sector show the urgent need not only for reform of the regulatory system but also for an overhaul of how these institutions operate.

So far, a handful of banks – including Barclays, HSBC, and Coutts – have been fined more than US$500 million in the past 12 months for misconduct. This sounds impressive until it’s compared to the US$8.5 trillion in assets that just five leading banks held at the end of 2011, or the half-year profits reported this year. Although banks under scrutiny are putting aside funds to take care of fines and possible lawsuits, Barclays Bank and HSBC alone reported more than US$17 billion in pre-tax profits for the first six months of this year.

Corruption and tolerance for unethical behavior are at the root of the illegal activities that have damaged the livelihoods of millions of people and the reputation of the financial industry as a whole. This has to change. If you rely and on FDIC to protect your best interest at a bank, take a close look at what bank partners in crime have to offer… Michael Huke a senior manager at Lloyds Bank HQ Bristol, a record of his nefarious activities, each reported to Lloyds Bank and Avon and Somerset police where applicable, NO action has been taken by either party.

Michael Huke’ on YouTube witness his disgraceful conduct.

1. CCTV of Michael Huke shouting abuse and videoing his neighbors within their premises.

2. Assaulting neighbors physically and verbally, captured on CCTV and audio.

3. Offensive and unlawful TEXTs sent by Michael Huke……..

a) TEXT ‘My secretary gives me a blow job when I’m allocating bonuses

b) TEXT ‘Kompany and Fernandinho (Manchester City footballers) are Northern black c*nts’.

c) TEXT ‘Antonio Horta Osario (Lloyds Bank CEO) has no balls because he was off sick at the priory for 6 months’ suffering from a nervous breakdown.

d) TEXT claiming ‘He would wind up 2 neighbors (he was hostile towards) so much, he would let them Twat him and get them done’. Plus more TEXTs of a similar grossly offensive nature.

4. When asked by friends the wealth of a landlord neighbor (that he was in conflict with), he answered ‘neither the landlord or his wife bank with Lloyds Banking Group and never have had accounts with us’. Within his ‘position of trust’ how did he determine that information, had they banked with Lloyds he would surely have probed their accounts?

5. He was prosecuted, when caught on covert CCTV, watching his dog defecate outside a neighbor’s property and not clear it up.

6. He signed an ABC (Acceptable Behaviour Contract) issued to him by South Gloucestershire Council ASBO team.

7. Attacked a 71-year-old man because he’d parked briefly on the road outside his house; captured on CCTV, video/audio recorded and independently witnessed (view on YouTube).

8. The 71-year-old victim of the attack and one of the witnesses (who’d videoed the attack) were arrested and held in custody (several months after the video of the attack had been uploaded onto YouTube, (by persons unknown), charged with uploading the video, (which was factual and not menacing in character) as it discredited Michael Huke in front of his staff and jeopardized his job at Lloyds Bank HQ Bristol. No charge was pursued. This arrest was almost certainly influenced by Lloyds Banking Group, Freemasons, a police sergeant friend who lives nearby or corrupt members of Avon and Somerset Police, possibly a combination of them all.

Since the above, he works from home one or two days each week spending time at the sports center and maintaining his property and garden!

These incidents plus many more have taken place over a 3 year period; all reported to Lloyds Banking Group, yet Michael Huke is still an employee of Lloyds Bank?

Views, opinions, advice would be greatly appreciated.

You’re protected from losses if your FDIC-insured bank goes belly-up, assuming your funds are in qualifying accounts and fall below the maximum limits.

Although banks are a safe place for your money, they do lend your money out and invest it to earn a profit. If these investments go sour, what happens to your money?

If your account is fully insured, you’re in pretty good shape. The FDIC will make you whole by replacing your funds or sending money to you. However, FDIC coverage has limits. Certain types of accounts are not insured, and you’re only covered up to $250,000 per depositor per bank. You can get additional coverage at a single bank depending on a number of factors, including how your accounts are titled. Read More

Between the bank’s lawyers and FDIC, you’ll need GOD to be protected

As she says, these services are all readily available in the world’s biggest international financial centres, like Singapore, London or New York, as well as smaller tax havens and secrecy jurisdictions. It’s very easy to set up layers of paper companies and trusts to cover your tracks. Banks too often fail to do the proper checks on suspect clients or funds, and regulators don’t punish them for these failures. Without this kind of complicity from the international system, crime and corruption of this kind would be much harder to get away with.

When citizens get so fed up with the state-looting they pour out onto the streets in protest, as seen recently in Libya or Ukraine, and governments are quick to freeze assets. But the headlines about expensive private homes, huge bank accounts and glamorous double lives of newly fallen dictators in Western hotspots point to a more fundamental problem. If corruption is so obvious, what is the money doing there in the first place?

Global Witness wants to change this. We want a world in which business is done in the open and for the greater good. That’s why our investigations and advocacy focus on changing the international systems which make corruption and money laundering possible. We’re calling for international public registries of the real owners of companies, visa bans for corrupt politicians, better regulation of banks and lawyers and strict enforcement of anti-money laundering laws. Source

List of international bank acquisitions Announcement date Target Acquirer Transaction Value US$ billion) 9-10-2007 Netherlands ABN AMRO United Kingdom Royal Bank of Scotland Belgium Fortis Spain Santander 77.230 22-2-2008 United Kingdom Northern Rock United Kingdom Government of the United Kingdom 41.213 1-4-2008 United States Bear Stearns United States JPMorgan 2.200 1-7-2008 United States Countrywide Financial United States Bank of America 4.000 14-7-2008 United Kingdom Alliance & Leicester Spain Santander 1.930 31-8-2008 Germany Dresdner Kleinwort Germany Commerzbank 10.812 7-9-2008 United States Fannie Mae and Freddie Mac United States Federal Housing Finance Agency 5,000.000 14-9-2008 United States Merrill Lynch United States Bank of America 44.000 16-9-2008 United States American International Group United States United States Treasury 182.000 17-9-2008 United States Lehman Brothers United Kingdom Barclays 1.300 18-9-2008 United Kingdom HBOS United Kingdom Lloyds TSB 33.475 26-9-2008 United States Lehman Brothers Japan Nomura Holdings 1.300 26-9-2008 United States Washington Mutual United States JPMorgan 1.900 28-9-2008 United Kingdom Bradford & Bingley United Kingdom Government of the United Kingdom Spain Santander 1.838 28-9-2008 Belgium Luxembourg Netherlands Fortis France BNP Paribas 12.356 29-9-2008 United Kingdom Abbey National United Kingdom Government of the United Kingdom Spain Santander 2.298 30-9-2008 Belgium Dexia Belgium France Luxembourg The Governments of Belgium, France and Luxembourg 7.060 3-10-2008 United States Wachovia United States Wells Fargo 15.000 7-10-2008 Iceland Landsbanki Iceland Icelandic Financial Supervisory Authority 4.192 8-10-2008 Iceland Glitnir Iceland Icelandic Financial Supervisory Authority 3.254 9-10-2008 Iceland Kaupthing Bank Iceland Icelandic Financial Supervisory Authority 1.257 13-10-2008 United Kingdom Lloyds Banking Group United Kingdom Government of the United Kingdom 26.045 13-10-2008 United Kingdom Royal Bank of Scotland Group United Kingdom Government of the United Kingdom 30.641 14-10-2008 United States Bank of America United States United States Federal Government 45.000 14-10-2008 United States Bank of New York Mellon United States United States Federal Government 3.000 14-10-2008 United States Goldman Sachs United States United States Federal Government 10.000 14-10-2008 United States JP Morgan United States United States Federal Government 25.000 14-10-2008 United States Morgan Stanley United States United States Federal Government 10.000 14-10-2008 United States State Street United States United States Federal Government 2.000 14-10-2008 United States Wells Fargo United States United States Federal Government 25.000 17-10-2008 Switzerland UBS Switzerland Swiss National Bank 65.314 22-10-2008 Netherlands ING Group Netherlands Government of the Netherlands 11.032 23-11-2008 United States Citigroup United States United States Federal Government 300.000 11-2-2009 Republic of Ireland Allied Irish Bank Republic of Ireland Government of the Republic of Ireland 3.861 11-2-2009 Republic of Ireland Anglo Irish Bank Republic of Ireland Government of the Republic of Ireland 13.570 11-2-2009 Republic of Ireland Bank of Ireland Republic of Ireland Government of the Republic of Ireland 3.861 13-3-2012 Greece Alpha Bank Greece Government of Greece 2.096 13-3-2012 Greece Eurobank Greece Government of Greece 4.633 13-3-2012 Greece National Bank of Greece Greece Government of Greece 7.612 13-3-2012 Greece Piraeus Bank Greece Government of Greece 5.516 25-3-2012 Cyprus Laiki Bank Cyprus Bank of Cyprus 10.812 25-5-2012 Spain Bankia Spain Government of Spain 20.962 7-6-2012 Portugal Caixa Geral de Depositos Portugal Government of Portugal 1.780 7-6-2012 Portugal Millennium BCP Portugal Government of Portugal 3.300 Bank failures in the U.S. In the U.S., deposits in savings and checking accounts are backed by the FDIC. Currently, each account owner is insured up to $250,000 in the event of a bank failure.[4] When a bank fails, in addition to insuring the deposits, the FDIC acts as the receiver of the failed bank, taking control of the bank’s assets and deciding how to settle its debts. The number of bank failures is tracked and published by the FDIC since 1934 and has decreased after a peak in 2010 due to the financial crisis of 2007–08.[5] No advance notice is given to the public when a bank fails.[6] Under ideal circumstances, a bank failure can occur without customers losing access to their funds at any point. For example, in the 2008 failure of Washington Mutual the FDIC was able to broker a deal in which JP Morgan Chase bought the assets of Washington Mutual for $1.9 billion.[7] Existing customers were immediately turned into JP Morgan Chase customers, without disruption in their ability to use their ATM cards or do banking at branches.[8] Such policies are designed to discourage bank runs that might cause economic damage on a wider scale.“Bank panic” redirects here. For the video game, see Bank Panic.

American Union Bank, New York City. April 26, 1932.

A bank run (also known as a run on the bank) occurs when a large number of people withdraw their money from a bank because they believe the bank may cease to function in the near future. In other words, it is when, in a fractional-reserve banking system (where banks normally only keep a small proportion of their assets as cash), a large number of customers withdraw cash from deposit accounts with a financial institution at the same time because they believe that the financial institution is, or might become, insolvent; they keep the cash or transfer it into other assets, such as government bonds, precious metals or gemstones. When they transfer funds to another institution, it may be characterized as a capital flight. As a bank run progresses, it generates its own momentum: as more people withdraw cash, the likelihood of default increases, triggering further withdrawals. This can destabilize the bank to the point where it runs out of cash and thus faces sudden bankruptcy.[1] To combat a bank run, a bank may limit how much cash each customer may withdraw, suspend withdrawals altogether, or promptly acquire more cash from other banks or from the central bank, besides other measures.

A banking panic or bank panic is a financial crisis that occurs when many banks suffer runs at the same time, as people suddenly try to convert their threatened deposits into cash or try to get out of their domestic banking system altogether. A systemic banking crisis is one where all or almost all of the banking capital in a country is wiped out.[2] The resulting chain of bankruptcies can cause a long economic recession as domestic businesses and consumers are starved of capital as the domestic banking system shuts down.[3] According to former U.S. Federal Reserve chairman Ben Bernanke, the Great Depression was caused by the Federal Reserve System,[4] and much of the economic damage was caused directly by bank runs.[5] The cost of cleaning up a systemic banking crisis can be huge, with fiscal costs averaging 13% of GDP and economic output losses averaging 20% of GDP for important crises from 1970 to 2007.[2]

Several techniques have been used to try to prevent bank runs or mitigate their effects. They have included a higher reserve requirement (requiring banks to keep more of their reserves as cash), government bailouts of banks, supervision and regulation of commercial banks, the organization of central banks that act as a lender of last resort, the protection of deposit insurance systems such as the U.S. Federal Deposit Insurance Corporation,[1] and after a run has started, a temporary suspension of withdrawals.[6] These techniques do not always work: for example, even with deposit insurance, depositors may still be motivated by beliefs they may lack immediate access to deposits during a bank reorganization.[7]

Christians are in a parallel situation. The life, death, and resurrection of Jesus have paid our sin debt to God. Now, as we have the opportunity, we can help others in need, particularly fellow believers, with loans that do not escalate their troubles. Jesus even gave a parable along these lines about two creditors and their attitude toward forgiveness (Matthew 18:23-35).

The Bible neither expressly forbids nor condones the borrowing of money. The wisdom of the Bible teaches us that it is usually not a good idea to go into debt. Debt essentially makes us a slave to the one who provides the loan. At the same time, in some situations going into debt is a “necessary evil.” As long as money is being handled wisely and the debt payments are manageable, a Christian can take on the burden of financial debt if it is absolutely necessary.

StevieRay Hansen

Editor, Bankster Crime

MY MISSION IS NOT TO CONVINCE YOU, ONLY TO INFORM…

#Fraud #Banks #Money #Corruption #Bankers

![]()

Michael Huke a senior manager at Lloyds Bank HQ Bristol, a record of his nefarious activities, each reported to Lloyds Bank and Avon and Somerset police where applicable, NO action has been taken by either party.

Please view ‘Michael Huke’ on YouTube and witness his disgraceful conduct.

1. CCTV of Michael Huke shouting abuse and videoing his neighbours within their premises.

2. Assaulting neighbours physically and verbally, captured on CCTV and audio.

3. Offensive and unlawful TEXTs sent by Michael Huke……..

a) TEXT ‘My secretary gives me a blow job when I’m allocating bonuses

b) TEXT ‘Kompany and Fernandinho (Manchester City footballers) are Northern black c*nts’.

c) TEXT ‘Antonio Horta Osario (Lloyds Bank CEO) has no balls because he was off sick at the priory for 6 months’ suffering from a nervous breakdown.

d) TEXT claiming ‘He would wind up 2 neighbours (he was hostile towards) so much, he would let them Twat him and get them done’. Plus more TEXTs of a similar grossly offensive nature.

4. When asked by friends the wealth of a landlord neighbour (that he was in conflict with), he answered ‘neither the landlord or his wife bank with Lloyds Banking Group and never have had accounts with us’. Within his ‘position of trust’ how did he determine that information, had they banked with Lloyds he would surely have probed their accounts?

5. He was prosecuted, when caught on covert CCTV, watching his dog defecate outside a neighbour’s property and not clear it up.

6. He signed an ABC (Acceptable Behaviour Contract) issued to him by South Gloucestershire Council ASBO team.

7. Attacked a 71 year old man because he’d parked briefly on the road outside his house; captured on CCTV, video/audio recorded and independently witnessed (view on YouTube).

8. The 71 year old victim of the attack and one of the witness’s (who’d videoed the attack) were arrested and held in custody (several months after the video of the attack had been uploaded onto YouTube, (by persons unknown), charged with uploading the video, (which was factual and not menacing in character) as it discredited Michael Huke in front of his staff and jeopardised his job at Lloyds Bank HQ Bristol. No charge was pursued. This arrest was almost certainly influenced by Lloyds Banking Group, Freemasons, a police sergeant friend who lives nearby or corrupt members of Avon and Somerset Police, possibly a combination of them all.

Since the above he works from home one or two days each week spending time at the sports centre and maintaining his property and garden!

These incidents plus many more have taken place over a 3 year period; all reported to Lloyds Banking Group, yet Michael Huke is still an employee of Lloyds Bank?

You’re views, opinions, advice would be greatly appreciated.

Michael Huke manager at Lloyds Bank HQ Bristol

UPDATE…… Following this incident, the video/s (Michael Huke Lloyds Banker) were uploaded onto YouTube by one of the many people they had been forwarded too. 2 months later the person videoing the incident was arrested at his place of work, because Michael Huke the person rolling on the floor, claimed uploading the videos was harassment, as it made him look stupid/imbecilic and unprofessional in front of his staff which undermines and threatens his position as a manager at Lloyds Bank HQ Bristol. The arrested person initiated legal proceedings against Avon and Somerset Police for wrongful arrest, following court application the police released ‘Disclosure’ documents relating to their investigation, within these documents was a confession from Michael Huke that ‘he had not been attacked by the old man’ as he had reported to the police immediately after, and ‘had faked the attack’ in a vengeful attempt to get all parties into trouble. He also stated he was driving past on his way to the shops ‘he didn’t have any shoes on’, which indicates he was consumed with rage because the old man had parked outside his house so he scurried out to confront/attack him, forgetting his shoes. An out of court settlement was made by the police and accepted, the estimated cost to the police following this action is estimated at £150K. Michael Hukes actions ‘wasting police time’ and ‘perverting the course of justice’ are being investigated/processed and if proven/found guilty the later would almost certainly incur a custodial sentence, the police officer who made the arrest has since left the police force, Michael Huke has once again moved away to a nearby village.

Why is this man still employed by Lloyds Banking Group, surely all his staff are aware of the despicable activities he’s undertaken, (word travels fast in such circumstances) they can have no respect for him. Any other Bank or organisation upon being aware of and authenticated these activities would have dismissed him immediately. There are many more instances of him under ‘Michael Huke’ or Bad Bankers, or Bankers snooping etc.

Bravo for highlighting this man.