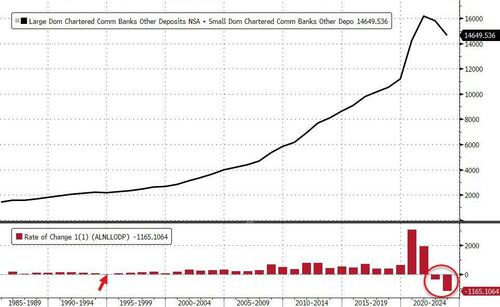

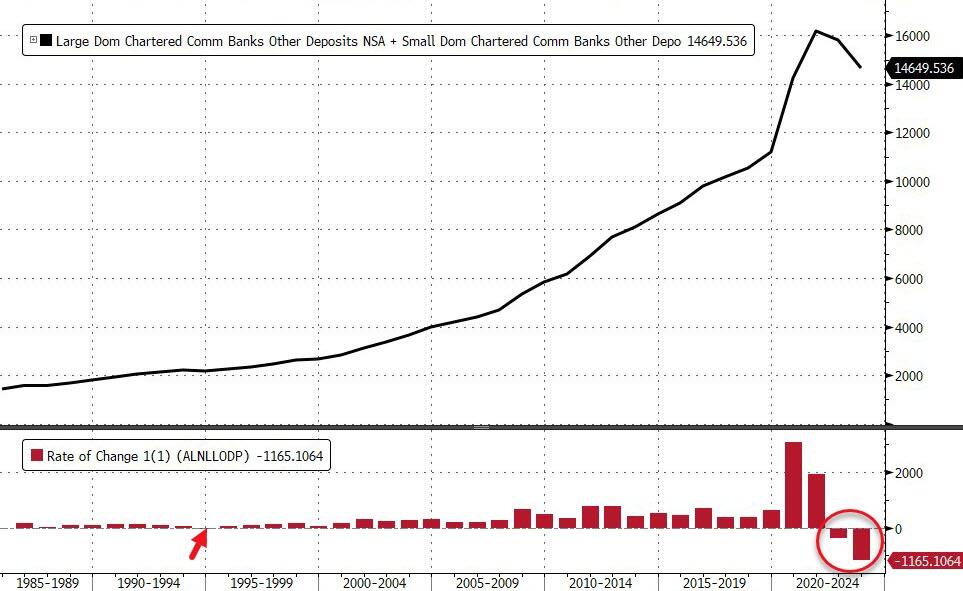

On a non-seasonally-adjusted basis (why adjust when we are looking at annual changes), US domestic banks saw a stunning $1.17TN in deposit outflows (ex-large time deposits) in 2023 – the largest annual decline ever (and only the 3rd annual decline on record going back to 1985 – 1994, 2022, and 2023)…

Source: Bloomberg

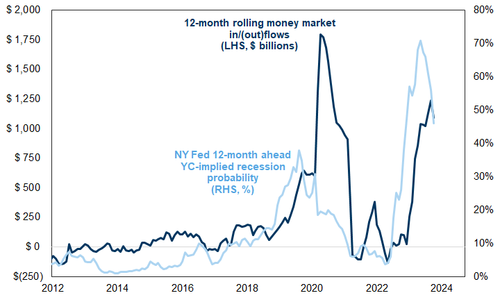

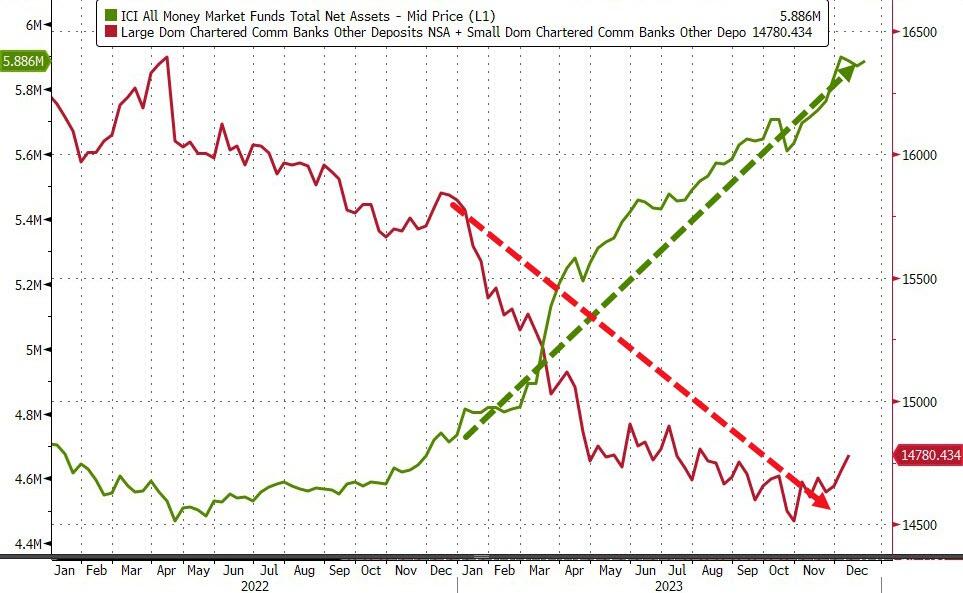

Interestingly, money-market funds saw inflows of around $1.15TN almost perfectly mirroring the deposit exodus from banks…

Source: Bloomberg

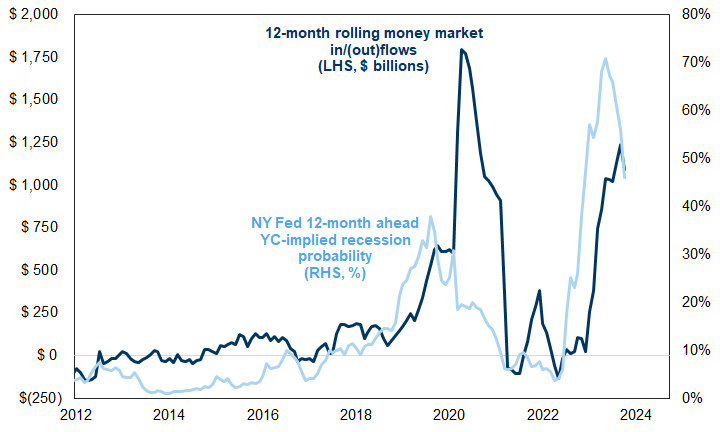

But, with recession odds declining rapidly, are we about to see MM outflows accelerate (and thus more deposit inflows – as we have seen in very recent weeks)?

Source: Goldman Sachs

Breaking down the outflows, it’s clear that large banks have suffered more pain in 2023:

Large Banks saw around $800BN in deposit outflows (ex-large time deposits) in 2023 – the largest ever annual decline deposits and second year in a row (and only third year ever of annual deposit declines).

Small Banks saw around $300BN in deposit outflows (ex-large time deposits) in 2023 – the largest ever annual decline in deposits (actually the only annual decline in deposits ever in data going back to 1985.

A quick glance at the chart shows that despite the March event (which saw small bank deposits tumble – as they should after the bank failures), small banks continue to attract a lot of deposits.

Source: Bloomberg

For some reason, Americans hate giving their money to large banks, but it is small banks that are becoming dangerously under-capitalized as a result of having so many (relatively speaking) deposits.

The small bank deposit growth is happening as QT accelerates (green line above, down around $900BN in 2023) and even as the small banks themselves have little cash (as per the constraint chart below).

Small banks reserve ratio (blue line) continues to trend in a troubling direction, but excluding the $136BN from The Fed’s BTFP (red line), Small Banks are in big trouble – the crisis back (and large bank cash needs a home – green line – like picking up a small bank from the FDIC30

Source: Bloomberg

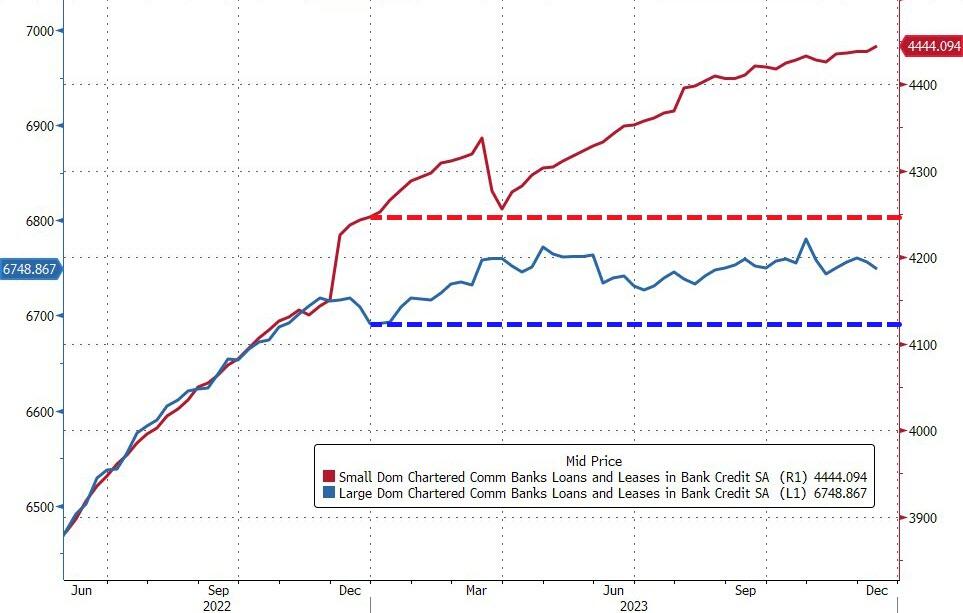

On the other side of the ledger, both Large and Small banks saw loan volumes increase on the year (as deposits fell), up $57BN (only) and $198BN respectively…

Source: Bloomberg

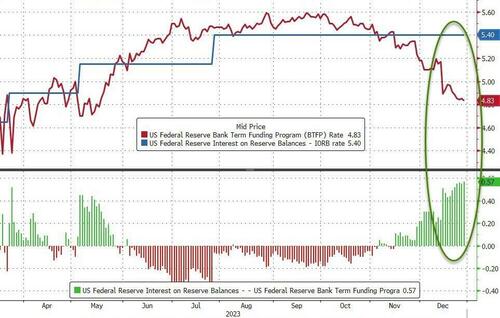

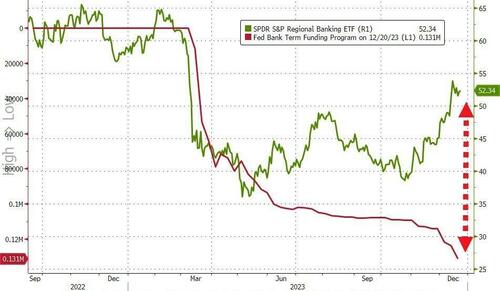

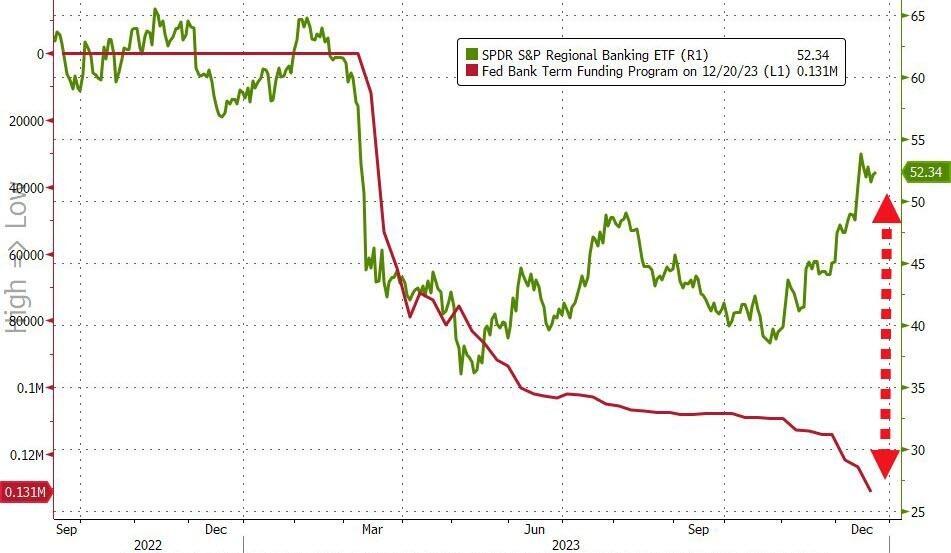

However, as we warned previously, the fallout from all this is that there is another pent up insolvency brewing – especially if The Fed proceeds with terminating its BTFP bailout fund (which is now spewing free money to banks via arbitraging The Fed’s own various facilities) and reverse repo usage (a source of liquidity) falls to zero.

Don’t believe The Fed will kill the ‘temporary’ $136BN bailout facility, think again!

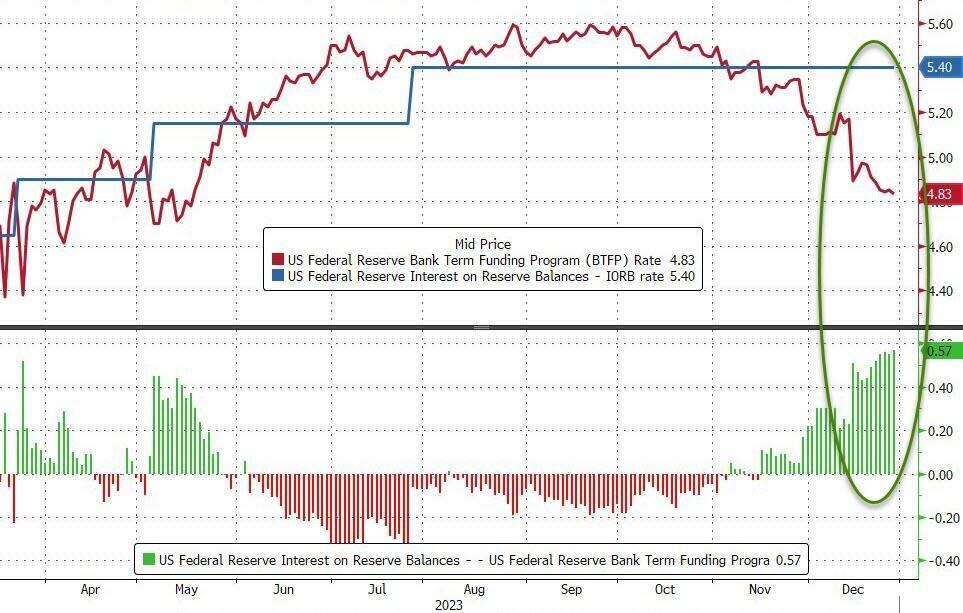

As a reminder, the growing gap between the rate on the Federal Reserve’s nascent funding facility and what the central bank pays institutions parking reserves suggests officials will let the program expire in March, according to Wrightson ICAP.

The rate on the Fed’s Bank Term Funding Program – which allows banks and credit unions to borrow funds for up to one year, pledging US Treasuries and agency debt as collateral valued at par – is the one-year overnight index swap rate plus 10 basis points.

That figure is currently 4.83%, down from 5.59% in September.

For institutions that have an account at the Fed, they can borrow from the BTFP at 4.83% and park that at the central bank to earn 5.40% – the interest on reserve balances.

Source: Bloomberg

The 57bp spread is the widest level since the Fed introduced the facility to support a struggling banking system after the collapse of California’s Silicon Valley Bank and Signature Bank in New York.

“In justifying the generous terms of the original program, the Fed cited the ‘unusual and exigent’ market conditions facing the banking industry following last spring’s deposit runs,” Wrightson ICAP economist Lou Crandall wrote in a note to clients.

“It would be difficult to defend a renewal in today’s more normal environment.”

Then WTF are banks going to do when The Fed shuts down this ‘temporary’ bailout program in March?

For now, investors are living on a prayer…

Happy New Year!

Treat your skin well. Our soaps are gentle and produce a smooth, creamy lather that is nourishing to your skin. They are handmade in small batches. We use only high-quality natural ingredients. No chemicals, no sodium laurel sulfate, no phthalates, no parabens, no detergents.GraniteRidgeSoapworks

The term double-minded comes from the Greek word dipsuchos, meaning “a person with two minds or souls.” It’s interesting that this word appears only in the book of…

Whether it is the civil war in Syria, the conflict between Russia and Ukraine, or the war against ISIS/ISIL, no conflict today is necessarily a sign that the…

In his riveting memoir, "A Long Journey Home", StevieRay Hansen will lead you through his incredible journey from homeless kid to multimillionaire oilman willing to give a helping hand to other throwaway kids. Available on Amazon.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}