BanksterCrime:

“This problem seems likely, given the way Congress has behaved in recent years,” the Feds added.

The Federal Reserve is warning that the United States faces a “dollar inflation uncertainty nightmare,” or hyperinflation in other words.

It is no secret that the U.S. dollar’s purchasing power has vastly been diminished annually. To put things in perspective, in 1913 $1 could have purchases 30 Hershey’s chocolate bars. Now $1 cannot even buy one.

Moreover, according to the CPI Inflation Calculator, the buying power of $1 now equates to $24.26 in order to adjust for inflation, per the charts below

But now the Federal Reserve is warning that dollar inflation has the potential to become exponentially worse.

Receiving no press time in the mainstream and alternative media, on June 2nd, the Federal Reserve of St. Louis published a financial report titled “Fiscal Dominance and the Return of Zero-Interest Bank Reserve Requirements.”

According to the paper’s abstract:

As a matter of arithmetic, the trends of US government debt and deficits will eventually result in an outrageously high government debt-to-GDP ratio. But when exactly will the United States hit the constraint of infeasibility and how exactly will policy adjust to it?

This article considers fiscal dominance, which is the possibility that accumulating government debt and deficits can produce increases in inflation that “dominate” central bank intentions to keep inflation low.

Is it a serious possibility for the United States in the near future? And how might various policies change (especially those related to the banking system) if fiscal dominance became a reality?

Furthermore, the Federal Reserve adds, “The essence of fiscal dominance is the need for the government to fund its deficits on the margin with non-interest-bearing debts. The use of non-interest-bearing debt as a means of funding is also known as “inflation taxation.” Fiscal dominance leads governments to rely on inflation taxation by “printing money” (increasing the supply of non-interest-bearing government debt).”

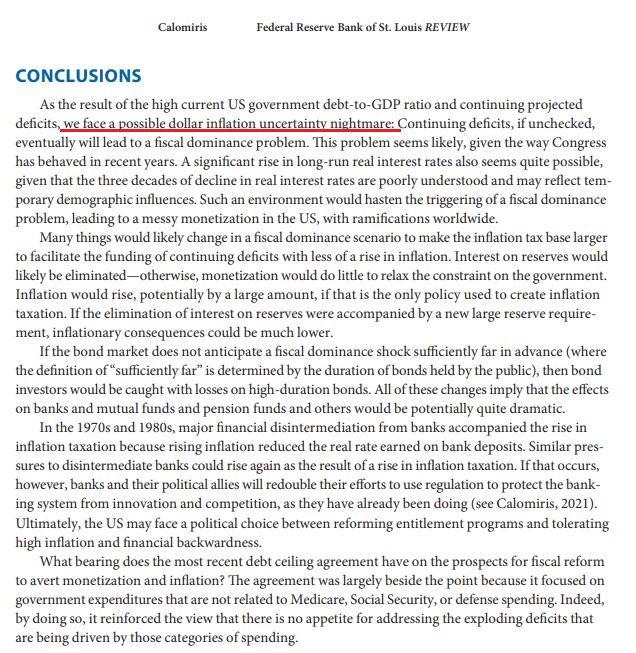

But to make a long story short, the St. Louis branch of the Federal Reserve offered their conclusion on the matter, warning that “we face a possible dollar inflation uncertainty nightmare,” believing that this is “likely,” passing the blame on Congress and the federal government’s relentless spending.

The Feds wrote:

As the result of the high current US government debt-to-GDP ratio and continuing projected deficits, we face a possible dollar inflation uncertainty nightmare: Continuing deficits, if unchecked, eventually will lead to a fiscal dominance problem. This problem seems likely, given the way Congress has behaved in recent years. A significant rise in long-run real interest rates also seems quite possible, given that the three decades of decline in real interest rates are poorly understood and may reflect temporary demographic influences. Such an environment would hasten the triggering of a fiscal dominance problem, leading to a messy monetization in the US, with ramifications worldwide.

Many things would likely change in a fiscal dominance scenario to make the inflation tax base larger to facilitate the funding of continuing deficits with less of a rise in inflation. Interest on reserves would likely be eliminated—otherwise, monetization would do little to relax the constraint on the government. Inflation would rise, potentially by a large amount, if that is the only policy used to create inflation taxation. If the elimination of interest on reserves were accompanied by a new large reserve requirement, inflationary consequences could be much lower.

If the bond market does not anticipate a fiscal dominance shock sufficiently far in advance (where the definition of “sufficiently far” is determined by the duration of bonds held by the public), then bond investors would be caught with losses on high-duration bonds. All of these changes imply that the effects on banks and mutual funds and pension funds and others would be potentially quite dramatic.

In the 1970s and 1980s, major financial disintermediation from banks accompanied the rise in inflation taxation because rising inflation reduced the real rate earned on bank deposits. Similar pressures to disintermediate banks could rise again as the result of a rise in inflation taxation. If that occurs, however, banks and their political allies will redouble their efforts to use regulation to protect the bank- ing system from innovation and competition, as they have already been doing (see Calomiris, 2021). Ultimately, the US may face a political choice between reforming entitlement programs and tolerating high inflation and financial backwardness.

What bearing does the most recent debt ceiling agreement have on the prospects for fiscal reform to avert monetization and inflation? The agreement was largely beside the point because it focused on government expenditures that are not related to Medicare, Social Security, or defense spending. Indeed, by doing so, it reinforced the view that there is no appetite for addressing the exploding deficits that are being driven by those categories of spending.

AUTHOR COMMENTARY

In other words, the Federal Reserve is saying it is “likely” that the United States will turn into the Weimer Republic; where people are having to wheelbarrow their money to buy bread. And if they are saying it’s likely then you know it will happen eventually.

Of course, the Feds are trying to cover their rear-ends by passing the buck onto Congress. And while it is true that they, as we know, love to infinitely spend hand-over-fist and borrow into the now (i.e. raising the debt ceiling), the gaslighting from the Federal Reserve here is just unreal; for it is they that are the core of inflation, by printing all this funny money and inflating the money supply, whilst not mandating that the banks raise their capital reserve requirements, which would therefore contract the money supply and bring inflation to a crawl, but they don’t want you to know that.

The Federal Reserve is just trying to play the blame game and pass the buck onto other entities, so when the crap hits the fan they can say, ‘We told you so, in it’s the fine print, the devil is in the details, it’s not our fault you know.’ Absolutely disgusting.

SEE: Federal Reserve To Pump $2 Trillion Of Liquidity Into Economy To Keep The Ship Barely Afloat

The bottom line here is that, as I have repeatedly been warning about, inflation will only continue to get worse. I had written over a year ago that when these goonies at the Fed and government and media were talking about “transitory” inflation, and interest rates for salvation, I told people to disregard that because it would do nothing to stop inflation. The data we are getting is so fake it’s not even funny. I shop, you shop, and prices continue to vastly expand each month.

When the Federal Reserve moves to drop rates next year, you are going to see inflation once again really spike up in the run-up to the Presidential Clown Show, as both the dollar’s relative strength and actual parity dive some more.

Moreover, when all of these banks begin to fail later this year and next, after they start offloading their bonds and bad loans, and face the crunch of a collapsing real estate, housing, and auto loan, and credit market; the Feds will be right there to bail them with our money, per usual.

My advice to you is to continue to build reserves of food, water, clothes, ways to stay warm and cold from a decentralized source, have weapons and ammo, and keep your King James Bible tight; because we are headed into rough waters ahead and you don’t want to be caught napping.

By faith Noah, being warned of God of things not seen as yet, moved with fear, prepared an ark to the saving of his house; by the which he condemned the world, and became heir of the righteousness which is by faith.

Riches profit not in the day of wrath: but righteousness delivereth from death.

Hebrews 11:7; Proverbs 11:4

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

CLICK HERE TO DONATE

Be gentle with your skin. Our soaps are kind to your skin and create a creamy, silky lather that is nourishing. Small batches are made by hand. We only use the best natural ingredients. There are no chemicals, phthalates, parabens, sodium laurel sulfate, or detergents. GraniteRidgeSoapworks

Use the code HNEWS10 to receive 10% off your first purchase.

Revelation: A Blueprint for the Great Tribulation

A Watchman Is Awakened

Will Putin Fulfill Biblical Prophecy and Attack Israel?