by Tyler Durden

AMs the dust settles on the SEC’s begrudging approval of spot bitcoin ETFs – and trading begins – the shitshow behind the scenes is becoming clearer as GBTC wins…

While Chair Gensler voted to approve the ETFs, he offered a personal statement worthy of the best cover-your-ass comment, warning that his decision in no way ‘approves bitcoin’ itself and that it’s a very scary place for investors full of terrorists, money-launderers, and drug-traffickers.

“While we approved the listing and trading of certain spot Bitcoin ETP shares today, we did not approve or endorse Bitcoin,” Gensler wrote.

“Investors should remain cautious about the myriad risks associated with Bitcoin and products whose value is tied to crypto.”

Was Gensler genuflecting to Liz Warren in hopes of repentance?

His comments were not missed by ArkInvest’s Cathie Wood:

“He just denigrated the whole crypto space. I couldn’t believe it,” Wood said in a Bloomberg Radio interview aired on X.

“This is par for the course in disruptive innovation.”

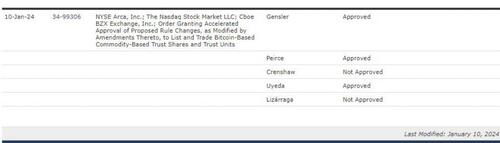

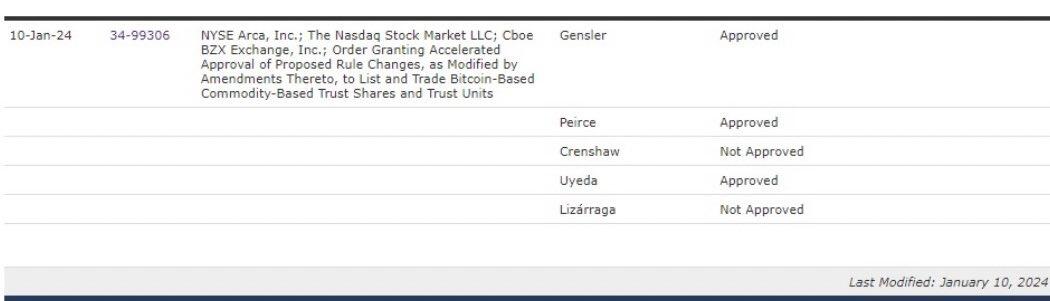

For some reason, the two Democratic SEC Commissioners chose to dissent, dis-approving of the ETFs…

Of course, their decision was not political at all – though they offered no rationale for their dissents.

Why would they be against the democratization?

Grzegorz Drozdz, market analyst for the European Union-based financial services platform Conotoxia commented that the general introduction of Bitcoin ETFs seems to have “significantly democratized” access to the market, “going beyond traditional cryptocurrency exchanges and wallets.”

Ah yes that’s why – because free-will and personal sovereignty are not part of the Marxist maxim preached from the left.

But it was Hester Peirce – so-called ‘Crypto Mom’ – that exposed the whole politcized farce in a wide-ranging rant statement after the vote.

Here it is in full (emphasis ours):

Today marks the end of an unnecessary, but consequential, saga. More than ten years after the filing of the first spot bitcoin exchange-traded product (“ETP”) application, the Commission finally has approved multiple applications by exchanges to allow the listing and trading of spot bitcoin ETPs. This saga likely would have spanned well beyond a decade were it not for the DC Circuit-ex-machina. You need not be a seasoned securities lawyer to spot the difference in treatment of bitcoin-related ETP applications compared to the many other ETP applications that have been routinely filed and approved over the past decade.

ETPs are an important innovation. Through them, investors can gain exposure to securities and non-securities, such as precious metals, in a convenient vehicle. Even if that exposure is available directly elsewhere, the ETP structure offers its own advantages. ETP shares trade continually on national stock exchanges at market prices, much as regular stocks do. By creating and redeeming shares of the fund, institutional traders, called authorized participants, help to maintain the price of these shares in line with the price of the assets in the investment pool. ETPs are accessible to investors and operate within the framework of the federal securities laws.

Since I became a Commissioner six years ago, one of the questions I have been asked most frequently is “When will the Commission approve a spot bitcoin ETP?” For reasons I have explained many times before, the logic of the long string of denials is perplexing. Predicting approval timelines for spot bitcoin ETPs was impossible because the review process for these filings did not resemble the fairly straightforward processes for approving comparable ETPs. The goalposts kept moving as the Commission slapped “DENIED” on application after application.

Bitcoin-based products have been trading for years under other regulatory regimes. In 2017, for example, the CME and the CBOE, which are regulated by the Commodity Futures Trading Commission, listed bitcoin futures. Foreign jurisdictions have long allowed spot bitcoin ETPs to trade. The Commission should have drawn comfort from the successful launch and smooth trading of these products, even through market stress and volatility. Instead, until today, the Commission remained steadfast in its unwillingness to let spot bitcoin ETPs into US markets.

In the meantime, the Commission has driven retail investors to less efficient means of attaining bitcoin exposure in the securities markets. For example, retail investors could hold it through non-exchange traded products or get some exposure by buying into companies or funds that owned or mined bitcoin. And, in 2021, bitcoin futures exchange-traded funds (“ETFs”), registered under the 1940 Act, started to trade given the Commission had no legal basis for stopping them. In 2022, the Commission approved the trading of bitcoin futures ETPs registered under the 1933 Act. These futures-based products are more complex and more difficult to manage than the spot product, which can translate into higher costs for investors. In any case, the Commission’s basis for letting these products trade should have been an equally compelling basis for letting spot products trade: the correlation between the bitcoin futures prices and the spot prices is high, which means that the regulated futures market is as relevant for a product based on spot bitcoin as it is for a fund investing in bitcoin futures. But, until a court reminded us that our “unexplained discounting of the obvious financial and mathematical relationship between the spot and futures markets falls short of the standard for reasoned decisionmaking,” we persisted in denying a spot bitcoin ETP.

The Commission, rather than admitting error, offers a weak explanation for its change of heart. In the past, the Commission, allowing our prejudice against the underlying asset to get in the way, has rejected applications on the basis that the bitcoin market was still immature and that there were outstanding manipulation concerns. Today’s approval order notes that the Commission now finds that means for “preventing fraud and manipulation” have been demonstrated because the prices on the CME bitcoin futures market and the spot bitcoin markets have been highly correlated throughout the past two-and-a-half years. We have denied multiple applications over that period, depriving investors of the opportunity to gain exposure to bitcoin in a more convenient and investor-friendly way. The only material change since we last denied a similar application was a judicial rebuke.

We squandered a decade of opportunities to do our job. If we had applied the standard we use for other commodity-based ETPs, we could have approved these products years ago, but we refused to do so until a court called our bluff. And even now our approval comes only begrudgingly, as demonstrated by our continued insistence that these products satisfy a correlation test we have not demanded of prior commodity-based ETPs. Perhaps the one silver lining here is now that we know that the Commission can execute a robust correlation analysis, perhaps the road to approving other spot crypto ETPs will not be as bumpy (even if the Commission insists on continuing to apply a test it applies nowhere else).

Today’s order does not undo the many harms created by the disparate treatment of spot bitcoin products.

- First, our arbitrary and capricious treatment of applications in this area will continue to harm our reputation far beyond crypto. Diminished trust from the public will inhibit our ability to regulate the markets effectively. This saga will taint future interactions between the industry and our staff and will dampen the rich, informative dialogue that best protects investors.

- Second, our disproportionate attention on these filings has diverted limited staff resources away from other mission critical work. Over ten years, likely millions of dollars of staff time has gone toward blocking these applications.

- Third, our actions here have muddied people’s understanding of what the SEC’s role is. Congress did not authorize us to tell people whether a particular investment is right for them, but we have abused administrative procedures to withhold investments that we do not like from the public.

- Fourth, by failing to follow our normal standards and processes in considering spot bitcoin ETPs, we have created an artificial frenzy around them. Had these products come to market in the way other comparable products typically have, we would have avoided the circus atmosphere in which we now find ourselves.

- Fifth, we have alienated a generation of product innovators within our space. Our unreasonable approach to these applications has signaled that regulatory prejudice against new products and services can lead us to sidestep the law and unreasonably delay product launches. The industry has logged hundreds of meetings, has filed submissions, withdrawals and amendments, and ultimately had to resort to a costly legal battle to get us to today.

Although this is a time for reflection, it is also a time for celebration. I am not celebrating bitcoin or bitcoin-related products; what one regulator thinks about bitcoin is irrelevant. I am celebrating the right of American investors to express their thoughts on bitcoin by buying and selling spot bitcoin ETPs. And I am celebrating the perseverance of market participants in trying to bring to market a product they think investors want. I commend applicants’ decade-long persistence in the face of the Commission’s obstruction.

Roughly translated, her message is clear…

width=550px

Weaponizing agencies? Politcized decision-making?

The ‘people’ seems happy as Bitcoin tops $49,000 and Ethereum rallies near $2700…

Source: Bloomberg

Be gentle with your skin. Our soaps are kind to your skin and create a creamy, silky lather that is nourishing. Small batches are made by hand. We only use the best natural ingredients. There are no chemicals, phthalates, parabens, sodium laurel sulfate, or detergents. GraniteRidgeSoapworks

To Get 20% Of Use Coupon Code Bankster20 Or HNews20

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}