BanksterCrime:

After JPMorgan Threatens to Sue, the Fed Cuts Its Capital Requirement on the 5-Count Felon from a Planned 25 Percent Hike to Less than 8 Percent…

By Pam Martens and Russ Martens,

It appears that Senator Elizabeth Warren was spot on in her assessment of the lack of a backbone for Federal Reserve Chairman Jerome Powell when it comes to raising capital requirements on the powerful megabanks on Wall Street. At a March 7 Senate Banking Committee hearing in which Powell was appearing as a witness, Warren said this:

“Despite all you said last year when the banks failed [in the spring banking crisis of 2023] about supporting Vice Chair Barr’s recommendations to strengthen rules for big banks, public reporting now says that you are driving efforts inside the Fed to weaken the capital rule. You even told the House Financial Services Committee representatives yesterday that you think it’s ‘very plausible’ that you withdraw the rule.”

The capital rule that Senator Warren is referring to was proposed more than a year ago by federal banking agencies but has yet to be enacted. It is formally known as the Basel III (or Basel Endgame) rule. Jamie Dimon, the Chairman and CEO of JPMorgan Chase, has been leading the charge to stop federal bank regulators from implementing the rule. (See Jamie Dimon Hires Dodd-Frank Hatchet Man to Weigh Suing the Fed Over Proposed Capital Rules.)

Warren concluded her comments to Powell at the March hearing with this:

“You are the leader of the Fed and when the heat was on last year, you talked a lot about getting tougher on the banks. But now the giant banks are unhappy about that and you’ve gone weak-kneed on this. The American people need a leader at the Fed who has the courage to stand up to these banks and protect our financial system.”

Dimon is aggressively fighting the rule change most likely because higher capital requirements could restrict the bank’s ability to prop up its share price with multi-billion-dollar stock buybacks each year, increase its dividend to appease its shareholders that this multi-felon bank is on the right course and lavish multi-million dollar bonuses on Dimon.

Powell has now demonstrated Senator Warren’s ability to correctly read the tea leaves. Quietly, at 5 p.m. last Wednesday, before the long Labor Day weekend, the Fed released its new capital requirements for the megabanks that will become effective on October 1, 2024.

We know that federal banking regulators had originally planned to increase JPMorgan Chase’s capital by 25 percent because Dimon stated that fact in his April letter to shareholders, writing that if the capital rules proposed by the FDIC, Office of the Comptroller of the Currency and the Federal Reserve are implemented, they “would increase our firm’s required capital by 25%.”

But instead of 25 percent, the Fed raised JPMorgan Chase’s capital requirement by just 7.89 percent from the 2023 level, taking it from a total capital requirement of 11.4 in 2023 to just 12.3 in 2024. Had the 25 percent increase been imposed, JPMorgan Chase’s capital requirement would have totaled 14.25.

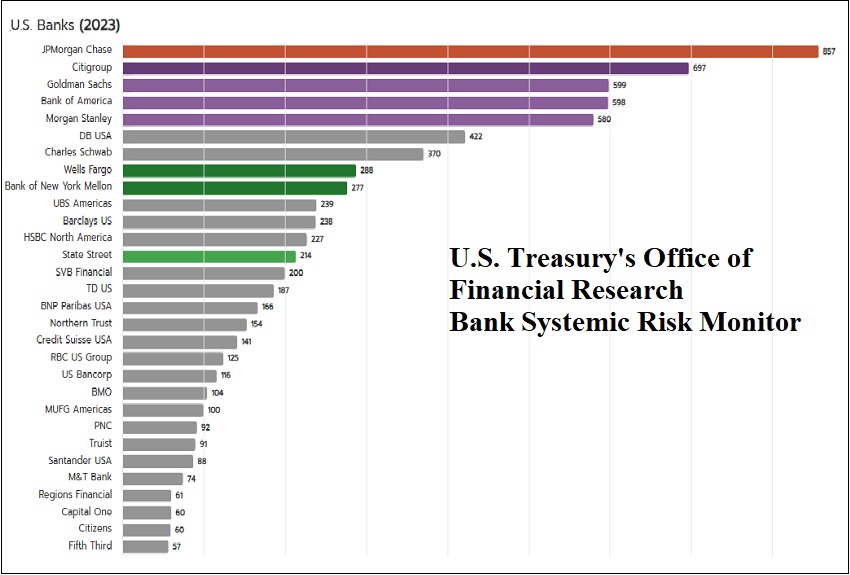

JPMorgan Chase is the largest U.S. bank and has for years been ranked by its regulators as – by far – the riskiest bank in the United States. The U.S. Treasury’s Office of Financial Research, which was created under the Dodd-Frank financial reform legislation of 2010 to provide federal regulators with up-to-date research on threats to financial stability, has created a “Bank Systemic Risk Monitor” that provides an overall score to show the systemic risk a particular bank represents to U.S. financial stability. The current chart is shown in the graph at the top of this article. JPMorgan Chase’s score of 857 is 23 percent higher than the next riskiest bank on the list, Citigroup, which has a systemic risk score of 697. (Citigroup is the bank that blew itself up in the financial crash of 2008 and received over $2.5 trillion in secret revolving loans from the Fed from December 2007 through July of 2010 according to the eventual audit released by the Government Accountability Office.)

But of particular note, JPMorgan Chase’s score is twice that of Deutsche Bank USA (DB USA), which has a systemic risk score of 422. And yet, here is what the Fed did last Wednesday. It raised Deutsche Bank USA’s capital requirement from 13.8 in 2023 to 18.4 currently – an increase of a whopping 33 percent versus an increase of 7.89 percent for JPMorgan Chase.

Jamie Dimon has been personally making the rounds in Washington in an effort to stop the implementation of the proposed capital rules. Internal government documents show that Dimon and his Chief of Staff, Judith Miller, met separately with the following Fed Governors on December 15 of last year: Fed Governor Adriana Kugler; Fed Vice Chair Philip Jefferson; and Fed Governor Christopher Waller.

Financial Times reporters Joshua Franklin and James Politi reported that in mid March, Dimon met in a one-on-one meeting with Vice President Kamala Harris and separately with President Biden’s Chief of Staff, Jeff Zients.

In a July 2 letter to Powell, Senator Warren described a “culture of corruption” that has taken root at the Fed since Powell became Chair. Among numerous issues, Warren cited the following:

“I am particularly concerned about reports that you have met or had private conversations with Jamie Dimon, the CEO of JPMorgan Chase, at least 19 times since becoming Chair of the Federal Reserve in February 2018. You have also reportedly met ten times with BlackRock CEO Larry Fink, seven times with Goldman Sachs CEO David Solomon, and at least nine times with the heads of other major banks. This is an astonishing amount of your time to give to the CEOs of the nation’s largest banks and financial firms.”

In addition to Warren, the watchdog group, Better Markets, has pushed back hard on the lies and fictions that the Wall Street megabanks are spreading in hopes of killing the more stringent capital rules. The YouTube video below features Better Markets’ Director of Banking Policy, Shayna Olesiuk, addressing those misleading claims.

![]()