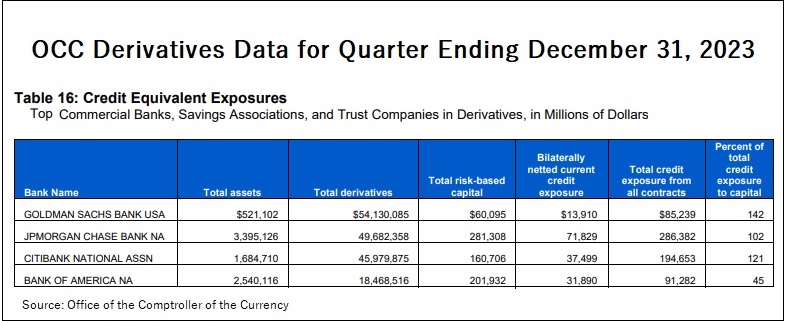

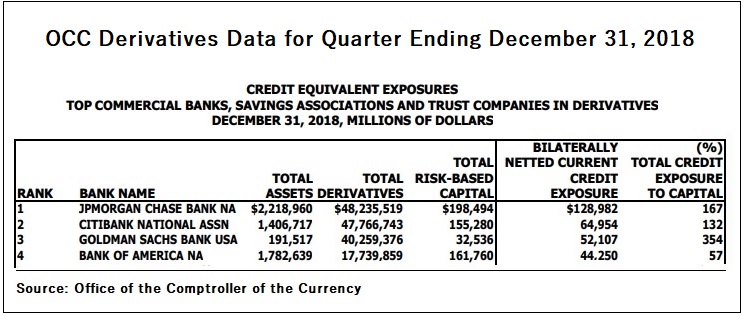

Goldman Sachs’ Bank Derivatives Have Grown from $40 Trillion to $54 Trillion in Five Years; So How Did Its Credit Exposure Improve by 200 Percent?

By BanksterCrime:

Source: Pam Martens and Russ Martens,

Last Friday, Goldman Sachs Bank USA, the federally-insured, U.S. taxpayer-backstopped commercial bank that the international trading behemoth, Goldman Sachs Group, is allowed to operate, got a smackdown from two of its regulators, the Federal Deposit Insurance Corporation (FDIC) and the Federal Reserve Board (the Fed).

The two regulators released a letter they had sent to David Solomon, Chairman and CEO of Goldman Sachs Group, which revealed that the commercial bank had flunked its wind-down test known as its “living will.” Derivatives were specifically cited for the “shortcomings.” Of particular note, the regulators wrote that Goldman Sachs Bank USA “…did not demonstrate the ability to model its derivatives portfolio unwind by counterparty for segmenting the portfolio in resolution. In the [upcoming] 2025 Plan, the Covered Company should demonstrate the ability to view derivatives positions at a counterparty level within both the portfolio unwind and segmentation capabilities.”

The above statement from regulators calls into serious question how Goldman Sachs Bank USA has been able to exponentially expand its derivatives from $40 trillion at the end of 2018 to $54 trillion at the end of last year but somehow reduce its ratio of credit exposure to capital from 354 percent for the quarter ending December 31, 2018 to 142 percent for the quarter ending December 31, 2023. (See charts above using data from the Office of the Comptroller of the Currency.)

Since knowing the risk of one’s counterparties is a key component of risk-weighting to determine capital needs, Goldman Sachs should have been able to “model its derivatives portfolio unwind by counterparty.”

The fact that it couldn’t raises more serious questions about regulator capture in the U.S.

For essential background, see our report: The Fed Has a Dirty Little Secret: It’s Been Allowing the Wall Street Mega Banks to Calculate their Own Capital Requirements.

Following the financial crash of 2008, Phil Angelides, the Chair of the Financial Crisis Inquiry Commission (FCIC), stated the following on June 30, 2010 at a hearing convened specifically to examine “The Role of Derivatives in the Financial Crisis”:

“I must say that despite 30 years in housing, finance, and investment — in both the public and private sectors — I had little appreciation of the tremendous leverage, risk, and speculation that was growing in the dark world of derivatives. Neither, apparently, did the captains of finance nor our leaders in Washington.

“The sheer size of the derivatives market is as stunning as its growth. The notional value of over the-counter derivatives grew from $88 trillion in 1999 to $684 trillion in 2008. That’s more than ten times the size of the Gross Domestic Product of all nations. Credit derivatives grew from less than a trillion dollars at the beginning of this decade to a peak of $58 trillion in 2007. These derivatives multiplied throughout our financial markets, unseen and unregulated…

“In June 2008, Goldman’s derivative book had a stunning notional value of $53 trillion.”

Today, after the much touted (but toothless) Dodd-Frank financial reform legislation of 2010, two more financial crises which included bailouts of Goldman Sachs and its peers, the derivatives book at Goldman is $1 trillion more than during the crisis of 2008 – the worst crisis since the Great Depression.

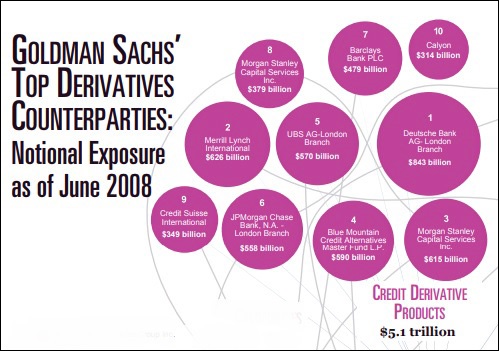

For why Goldman Sachs needs far more heightened scrutiny of its derivatives book than is currently happening, carefully consider the graph below which was released by the Financial Crisis Inquiry Commission that investigated the crash of 2008. The three largest counterparties to Goldman Sachs’ credit derivatives — Deutsche Bank, Merrill Lynch, and Morgan Stanley – all had to tap massive bailouts from the Fed.

Source: Financial Crisis Inquiry Commission

Largest Recipients of Federal Reserve Bailout Funds, 2007 to 2011

![]()

{kind=link}

{kind=link}