By Pam Martens and Russ Martens:

On Sunday, February 4, the CBS program 60 Minutes aired a taped interview with Federal Reserve Chairman Jerome Powell. The actual interview had occurred three days earlier and was conducted by 60 Minutes interviewer Scott Pelley. Two noteworthy things happened in connection with that interview: First, CBS did not indicate above the transcript of the interview that Powell’s comments had been materially shortened in the program that aired on TV; secondly, Powell calls the real estate problem at the largest banks “manageable” while shifting the more serious real estate loan problem to “smaller and regional banks.”

Below is what Powell had to say about problem real estate loans at U.S. banks in the 60 Minutes’ interview. The bracketed bold text is what is in the transcript but did not air in the broadcasted program on television. (Scroll to 8 minutes and 20 seconds at this link to listen to the relevant portion of the program that aired.)

PELLEY: The value of commercial office buildings all across the country is dropping as people work from home. Those buildings support the balance sheets of banks all across the country. What is the likelihood of another real estate-led banking crisis?

POWELL: I don’t think that’s likely. [So, what’s happening is, as you point out, we have work-from-home, and you have weakness in office real estate, and also retail, downtown retail. You have some of that. And there will be losses in that.] We looked at the larger banks’ balance sheets, and it appears to be a manageable problem. There’s some smaller and regional banks that have concentrated exposures in these areas that are challenged. And, you know we’re working with them. [This is something we’ve been aware of for, you know, a long time, and we’re working with them to make sure that they have the resources and a plan to work their way through the expected losses. There will be expected losses. It feels like a problem we’ll be working on for years. It’s a sizable problem. I don’t think — it doesn’t appear to have the makings of the kind of crisis things that we’ve seen sometimes in the past, for example, with the global financial crisis.]

More recently, on March 7 of last week, Powell appeared before the Senate Banking Committee to deliver his Semiannual Monetary Policy Report. In the Q&A that followed, Senator Catherine Cortez Masto (D-NV) raised the question with Powell on troubled real estate loans at U.S. banks. Cortez Masto said this:

CORTEZ MASTO: The Financial Stability Oversight Council’s 2023 report identified commercial real estate as a financial risk. And the Fed’s monetary report also noted commercial real estate prices continue to decline, especially in the office, retail, and multi-family sectors. I’m especially concerned that because of the low levels of transactions in the office sector, prices have not yet fully reflected the true decline in the value. So can you expand on the emerging risk the Federal Reserve has identified in the commercial real estate market – one – and then, I’m curious, can you discuss the compound risks identified in commercial real estate lending, particularly at banks with large CRE [Commercial Real Estate] concentrations and high fractions of uninsured deposits.”

As part of his answer, Powell again played down the real estate threat at the largest banks, stating: “There will be bank failures, but this is not the big banks. If you look at the very big banks, this is not a first order issue for any of the very large banks. It’s more smaller and medium size banks that have these issues.” (Watch the full exchange between Cortez Masto and Powell at one hour and 53 minutes (1:53) on the archived video here.)

According to Senator Elizabeth Warren, Powell is leading the charge behind the scenes to overturn federal regulators’ proposal to require the largest banks to hold larger amounts of capital. Downplaying the large banks’ risks from commercial real estate might be part of Powell’s overall agenda to gut the proposed capital rule.

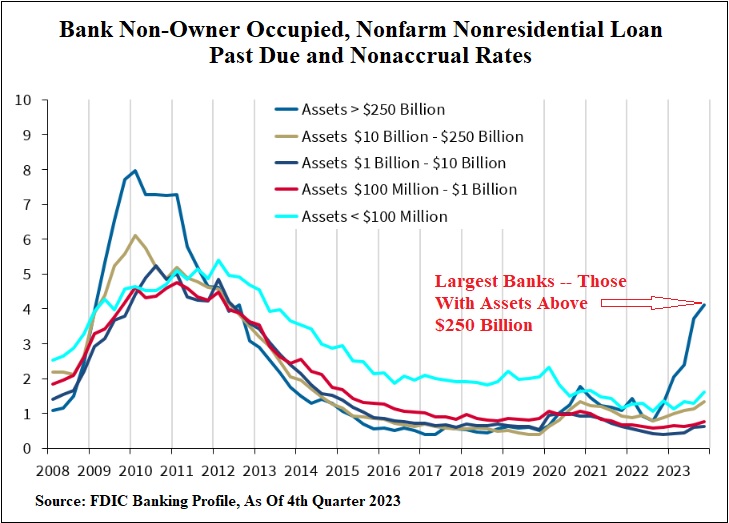

Powell has a long history of running interference for the mega banks on Wall Street (those that have combined federally-insured deposits with casino trading) and blaming the Fed’s serial and massive bailouts of these global behemoths on fanciful causes. Nonetheless, we were shocked when the Chair of the Federal Deposit Insurance Corporation (FDIC), Martin Gruenberg, held a press conference at the exact time last week that Powell was addressing the Senate Banking Committee. Gruenberg boldly announced a serious real estate problem inside the largest banks. Gruenberg’s press conference was to deliver the findings of the FDIC’s quarterly “Banking Profile.” Gruenberg stated the following: (Go to 5 minutes and 12 seconds at this link.)

GRUENBERG: “The increase in noncurrent loan balances was greatest among CRE [Commercial Real Estate] loans and credit cards. Weak demand for office space has softened property values and higher interest rates are affecting credit quality and refinancing ability of office and other types of CRE loans. As a result, the noncurrent rate for nonowner occupied CRE loans is now at its highest level since first quarter of 2014, driven by portfolios at the largest banks.” (Italic emphasis added.)

In fact, according to the chart above and accompanying data provided in an Excel spreadsheet by the FDIC, past due loans on commercial real estate at the largest banks (those with more than $250 billion in assets) as of December 31 of last year are at 4.11 percent. That’s 1.66 percent higher than at the end of the fourth quarter of 2008 when banks were exploding all over Wall Street during the financial crisis. As the chart above indicates, commercial real estate problems quickly became a lot worse at the largest banks, with the past due rate reaching 7.97 by the end of the first quarter of 2010.

That 4.11 percent past due rate at the biggest banks on December 31, 2023 compares with a past due rate of 1.35 percent at banks with $10 billion to $250 billion in assets, according to the latest FDIC bank profile data. Banks with $1 billion to $10 billion in assets have a negligible past due rate of 0.64 percent.

The title of the FDIC chart above is “Bank Non-Owner Occupied, Nonfarm Nonresidential Loan Past Due and Nonaccrual Rates.” The FDIC defines nonfarm nonresidential commercial properties as follows:

“loans secured by real estate as evidenced by mortgages or other liens on nonfarm nonresidential properties, including business and industrial properties, hotels, motels, churches, hospitals, educational and charitable institutions, dormitories, clubs, lodges, association buildings, ‘homes’ for aged persons and orphans, golf courses, recreational facilities, and similar properties.”

The FDIC defines “nonaccrual” status as follows:

“Nonaccrual — For purposes of this schedule, an asset is to be reported as being in nonaccrual status if: (1) it is maintained on a cash basis because of deterioration in the financial condition of the borrower, (2) payment in full of principal or interest is not expected, or (3) principal or interest has been in default for a period of 90 days or more unless the asset is both well secured and in the process of collection.”

The Fed is also doing something else related to growing losses at U.S. banks that is deeply concerning. It has stopped providing the aggregated quarterly data on the loan loss reserves at commercial banks – something it had previously done quarterly since 1984. The Fed data charts now come up with the words “DISCONTINUED.” (See here, here and here.) Our concern is that the largest banks are woefully under-reserved for their potential real estate losses.

Our Shampoo Bars are gentle and produce a nice lather that is nourishing to your hair. They are handmade in small batches. We use only high-quality natural ingredients that you can pronounce. No no single-use packaging waste. These are large bars (3.5 ounces) and will last about as long as 2 to 3 bottles of liquid shampoo, but without the plastic bottle that has been filled mostly with water. Also great for travel.

A lather can be built up in your hands and then applied to your hair, but it is best to rub the bar gently in your hair.

Birch Woods is a great outdoors-type scent. The notes are bergamot, patchouli, vetiver, and tonka bean.

Our Shampoo Bars are made with simple ingredients and scented only lightly with fragrance. The ingredients include glyceryl stearate, sodium cocoyl isethionate, propylene glycol, water, glycerin, fragrance oil, and mica colorants.

This listing is for 1 of our Shampoo Bars. A bar will weigh approximately 3.5 ounces and be approximately 2.5 inches across and 1 inch thick. Please keep in mind that our products are handmade and hand cut. Each bar is unique and might vary slightly in shape, size, design, and color from those pictured.

Please keep your Shampoo Bar well-drained and allow to dry between uses. This will ensure a longer lasting bar.

Allergen: Please test on a small area of skin prior to use and stop using if irritation occurs. Do not use if you are pregnant. Do not use on infants under the age of 24 months. Do not get shampoo in your eyes as it will sting slightly. Go Shopping